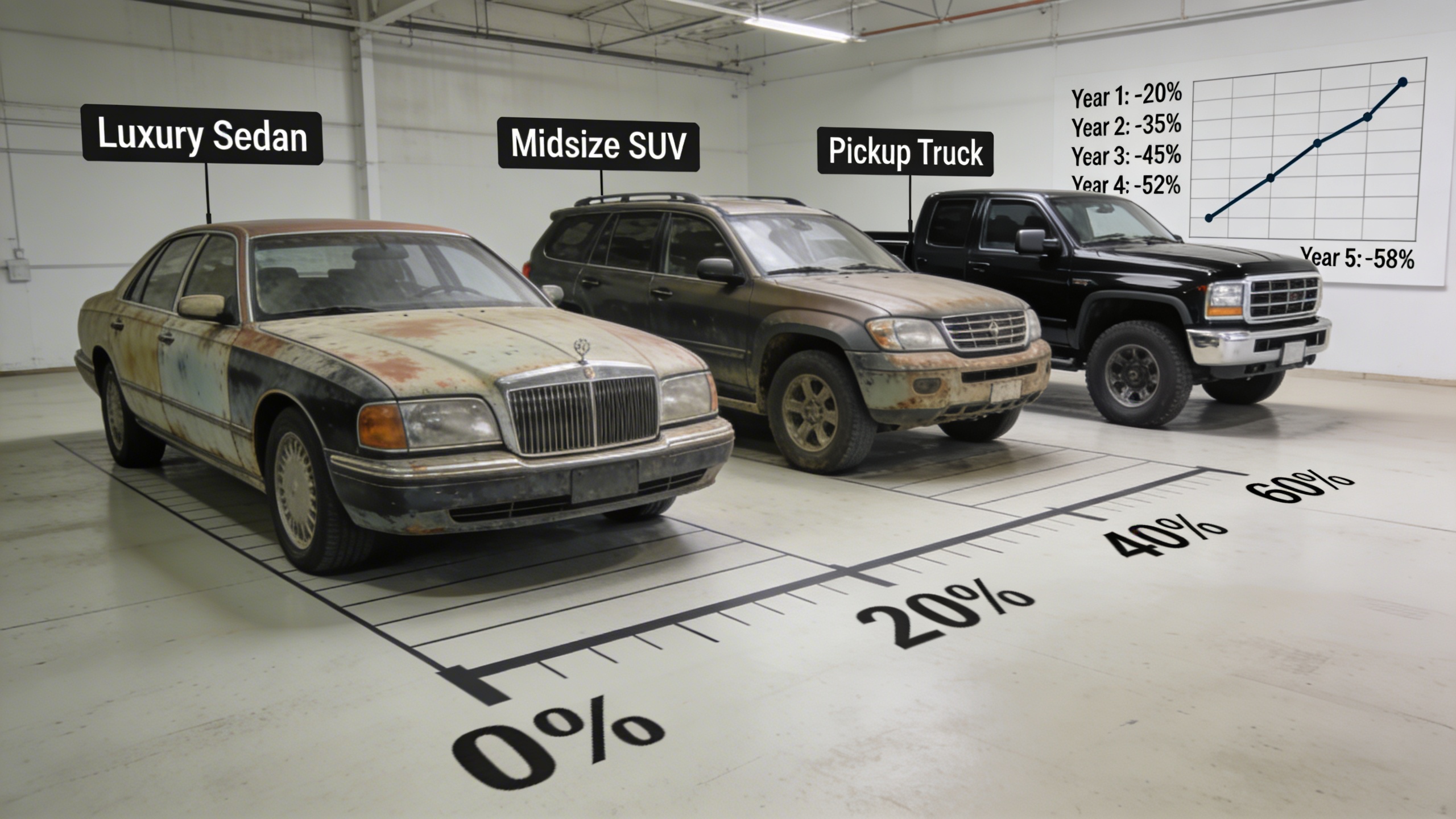

Sell your current car, buy the next one, don't get fleeced. That's the job. In a cooling U.S. used-vehicle market where inventories climbed and interest rates stayed stubbornly high, the choice between trading in and selling privately isn't trivial—it changes your net proceeds, your timeline, even your risk profile. And lurking beneath all of it's depreciation, the silent metronome that dictates how fast your equity evaporates. Let's dissect the decision with real numbers, USA-specific rules, and a clear plan you can execute this month.

The headline: private sales in the USA usually deliver 10–20% more than trade-ins, yet trade-ins often win on taxes, time, and liability. Your call depends on model demand, state regulations, and your appetite for handshakes with strangers in grocery store parking lots. There's nuance—lots of it.

During this, understanding depreciation—what actually moves those prices up or down—lets you time the market, pick vehicles that resist value loss, and decide whether a CarMax-style convenience play or a wholesale-minded route suits you best. And yes, there is a way to buy a car without a traditional dealership; the how matters.

Which Puts More Money in Your Pocket?

In most states, a clean private sale will net 10–20% more than a dealer trade-in. Why? Dealers need margin—typically 20–30%—to refurbish, floorplan, and warranty inventory. KBB and Edmunds trend lines show that a $25,000-market-value vehicle might yield a $22,000 trade credit, while a well-executed private listing can pull $24,000 to $26,000, assuming patience and proper marketing. Feels obvious. But zoom in on taxes and time, and it shifts.